In October 2024, the Singapore government accepted significant enhancements (opens a new window) to MediShield Life following a comprehensive review by the MediShield Life Council. These enhancements, which include higher benefit limits and coverage for new treatments like cell and gene therapy, are designed to shield citizens against the escalating costs of major health episodes.

However, this protection comes with a hefty price tag. To ensure the scheme’s long-term sustainability, the state approved premium increases up to 35%, to be phased in from April 2025 to March 2028. While a S$4.1 billion support package was deployed to cushion the impact for over 90% of Singaporeans, private sector organisations face a much harsher reality: they must navigate rising premiums and claims while simultaneously ensuring that their benefits programmes continue to position them as an employer of choice in an increasingly expensive talent market.

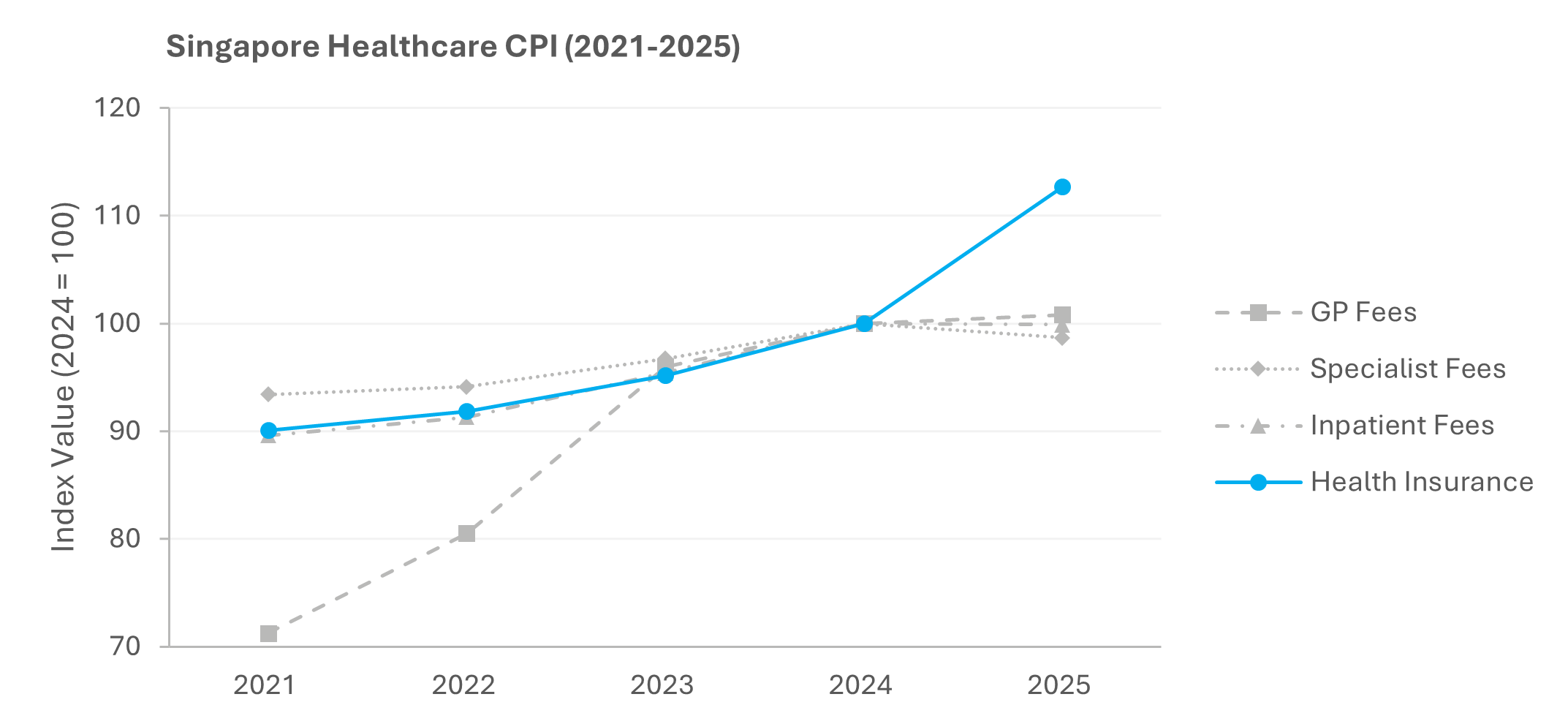

In November 2018, the Ministry of Health (MOH) began publishing private surgeon fee benchmarks to improve fee transparency and enable patients and payers to make informed decisions. Shortly afterwards, MOH mandated a minimum 5% co-payment on all Integrated Shield Plan (IP) riders sold from April 2019 onwards. From April 2026, IP riders are prohibited from covering minimum IP deductibles (opens a new window). Yet, despite years of interventions designed to curb over-consumption and keep healthcare affordable, the 12.7% spike in the 2025 Singapore Health Insurance Price Index was ultimately deemed a necessary adjustment for long-term sustainability.

For employers, the Singapore Health Insurance Price Index is merely a conservative estimate of the pressures they expect to face without government subsidies. Although the MOH has long established a payment hierarchy (opens a new window) where corporate insurance must act as the first payer before Integrated Shield Plans (IPs), MediShield Life, and MediSave are tapped, many employees might have historically claimed from IPs only out of convenience. Now that IP restrictions have taken effect, employees are incentivised to exhaust their corporate benefits to minimise MediSave and cash payments, putting additional pressure on already overstrained corporate benefits programmes.

Double-digit hikes well above this baseline are becoming the new, unavoidable norm. Unlike the State, private employers may lack the financial resources to absorb these costs indefinitely. Consequently, employers facing unsustainable increases can no longer afford to hesitate in implementing their own cost-containment measures. Co-payments, deductibles, panel network optimisation, and preventive health strategies – all of which have been heavily leveraged by the Singapore government – are quickly becoming essential tools for private employers to balance cost sustainability and benefit competitiveness.

Ultimately, the question for employers is no longer if they should adopt the government’s co-responsibility model, but how quickly they can implement a similar approach. Further delay will only lead to more painful, reactive cuts in the future.